Laws today aim to protect borrowers from discriminatory lending practices, but that wasn’t always the case. For decades, U.S. banks denied mortgages to Black applicants—and those belonging to other racial and ethnic minority groups—who lived in certain areas redlined by a federal agency called the Home Owners’ Loan Corp. (HOLC). Although HOLC has been defunct since the early 1950s, those practices still resonate today.

Key Takeaways

- Lending discrimination occurs when lenders base credit decisions on factors other than the applicant’s creditworthiness.

- Denying financial services to residents of certain neighborhoods due to race or ethnicity is commonly called redlining.

- The discriminatory practice of redlining made it impossible for many members of racial and ethnic minority groups to qualify for mortgages.

- Though now outlawed, redlining is one factor behind the racial wealth gap that persists in the United States today.

- Laws today forbid discrimination based on race, color, national origin, religion, sex, familial status, or disability.

Investopedia / Sabrina Jiang

What Is Lending Discrimination?

Lending discrimination occurs when lenders base credit decisions on factors other than a borrower’s creditworthiness. Today, three federal laws offer protection against such discrimination:

- The Fair Housing Act (FHA)

- The Equal Credit Opportunity Act (ECOA)

- The Community Reinvestment Act (CRA)

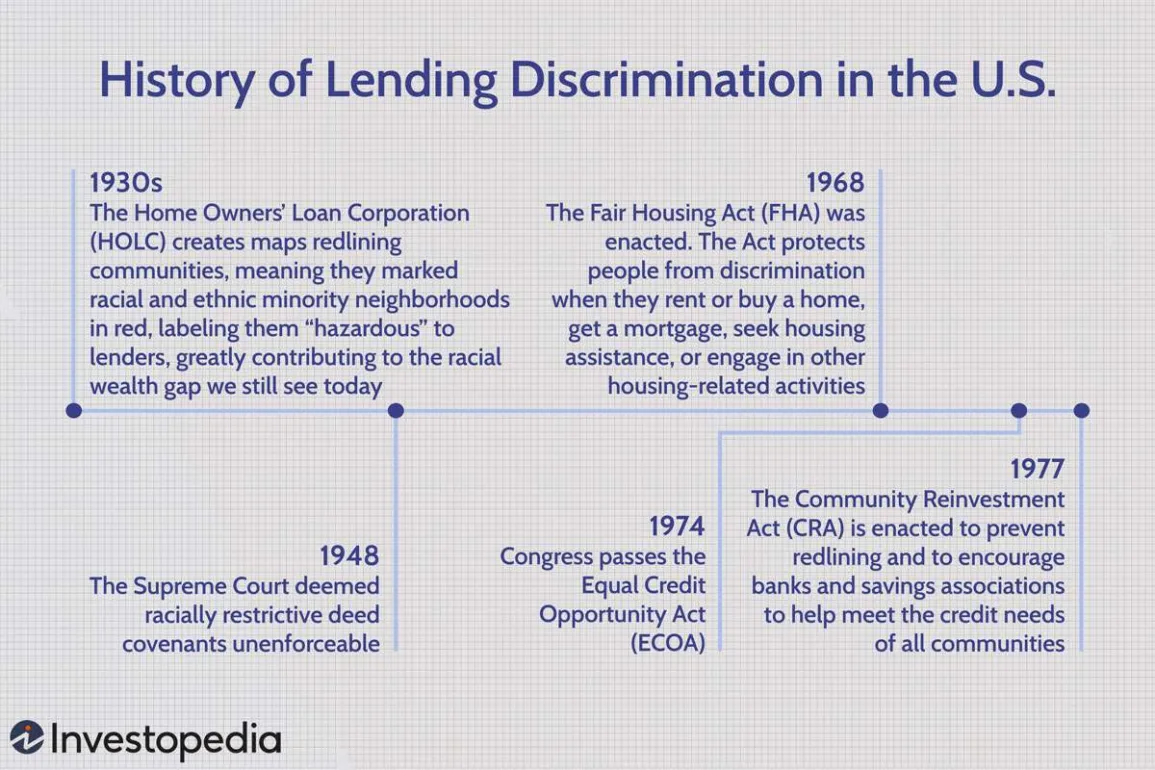

Fair Housing Act (FHA) of 1968

In 1948, the U.S. Supreme Court deemed racially restrictive deed covenants unenforceable. Twenty years later, the Fair Housing Act (FHA) was enacted. The law protects people from discrimination when they rent or buy a home, apply for a mortgage, seek housing assistance, or engage in other housing-related activities. It forbids discrimination based on race, color, national origin, religion, sex (including gender, gender identity, and sexual orientation), familial status, or disability during any part of a residential real estate transaction.

Equal Credit Opportunity Act (ECOA) of 1974

Discriminatory lending and housing practices continued despite the Fair Housing Act, and civil rights groups advocated for additional laws. In 1974, Congress passed the Equal Credit Opportunity Act (ECOA). According to the Federal Trade Commission, the ECOA “makes it illegal for creditors to discriminate based on race, color, religion, national origin, sex, marital status, age, or because all (or part) of a person’s income comes from public assistance.”

Creditors may ask for some of this information, but they can’t use it to deny you credit or establish the terms of your credit. For example, lenders can ask if you receive alimony or child support, but only if you need that income to qualify for the loan.

Community Reinvestment Act (CRA) of 1977

Even with the FHA and ECOA on the books, redlining continued in low- to moderate-income (LMI) neighborhoods. In its discussion of this period, the website Federal Reserve History notes, “There is some evidence that overt discrimination in mortgage lending persisted.”

A few things happened as a result:

- Illinois became the first state to pass a law prohibiting redlining, and it required banks to disclose their lending practices.

- Congress passed the Home Mortgage Disclosure Act (HMDA), which required banks to disclose the location of financed properties and the borrowers’ race and gender.

- Then-President Jimmy Carter signed into law the Community Reinvestment Act (CRA).

The CRA was enacted to prevent redlining and to encourage banks and savings associations to help meet the credit needs of all segments of their communities, including LMI neighborhoods. The law directed federal regulatory agencies to “(1) assess the institution’s record of meeting the credit needs of its entire community, including low- and moderate-income neighborhoods,” and “(2) take such record into account in its evaluation of an application for a deposit facility by such institution.”

What Is Redlining?

Before laws expressly prohibited discrimination in lending, the practice known as redlining prevented certain populations from accessing credit. Redlining is the discriminatory practice of denying financial services to residents of certain neighborhoods due to race or ethnicity.

Sociologist John McKnight coined the term in the 1960s, based on maps that marked racial and ethnic minority neighborhoods in red—labeling them “hazardous” to lenders. The maps were created by a federal agency, the Home Owners’ Loan Corp. (HOLC).

What the Home Owners’ Loan Corp. (HOLC) Did

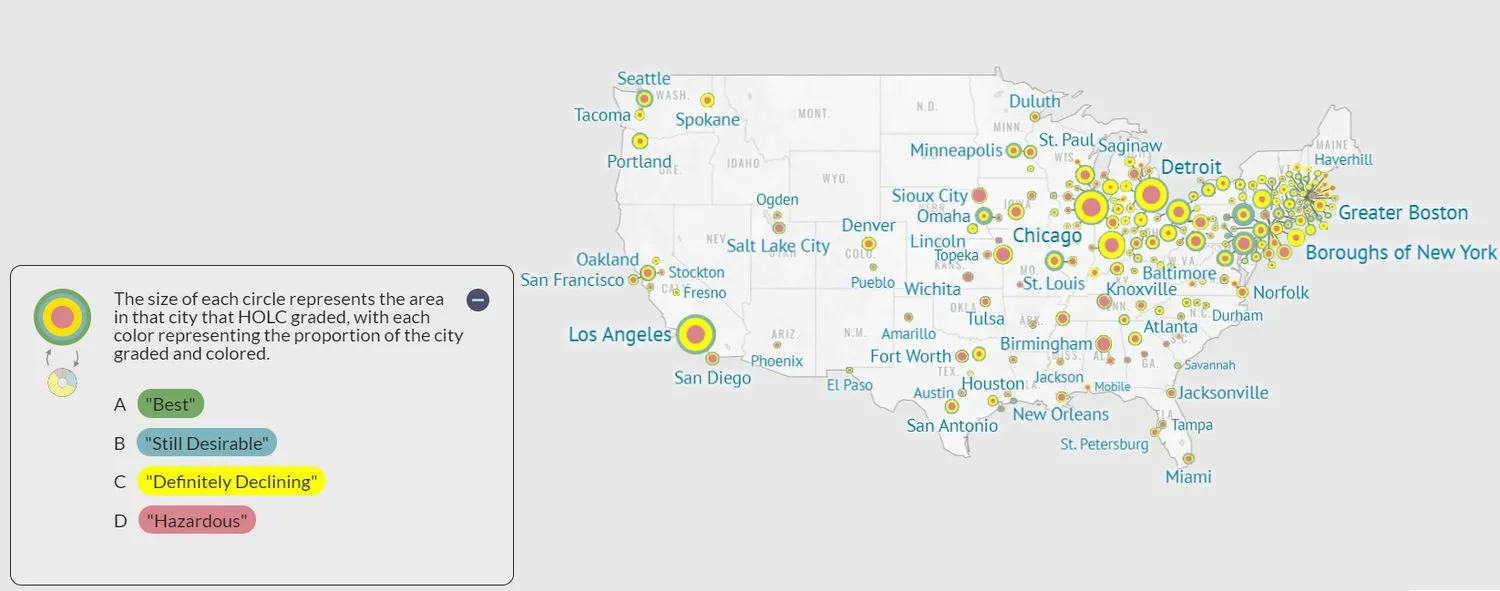

During the late 1930s, the HOLC—a federal agency—was created as part of the New Deal. The New Deal was a series of programs enacted under then-President Franklin Delano Roosevelt that were intended to help the U.S. recover from the Great Depression. The new agency’s purpose was to provide low-interest long-term mortgages to homeowners unable to obtain financing through normal banking channels. The HOLC drafted “Residential Security” maps of major cities as part of its City Survey Program.

To create the maps, HOLC examiners classified neighborhoods on a “perceived level of lending risk” using information gathered from local appraisers, bank loan officers, city officials, and real estate agents. According to the National Community Reinvestment Coalition, the examiners graded the neighborhoods based on factors including:

- The age and condition of the housing

- Access to transportation

- The closeness of popular amenities, such as parks

- Proximity to undesirable properties, such as polluting industries

- The residents’ economic class and employment status

- The residents’ ethnic and racial composition

The neighborhoods were color-coded on maps, with each color representing the area’s perceived risk to lenders.

| HOLC Maps Used in Redlining | ||

|---|---|---|

| Color | Grade | HOLC Description |

| Green | A “Best” | HOLC described A areas as “‘hot spots’…where good mortgage lenders with available funds are willing to make their maximum loans…—perhaps up to 75–80% of appraisal.” |

| Blue | B “Still Desirable” | HOLC described B areas as “still good” but not as “‘hot’ as A areas.” “They are neighborhoods where good mortgage lenders will have a tendency to hold commitments 10–15% under the limit,” or around 65% of appraisal. |

| Yellow | C “Definitely Declining” | C neighborhoods were characterized by “obsolescence [and] infiltration of lower grade population.” “Good mortgage lenders are more conservative in Third grade or C areas and hold commitments under the lending ratio for the A and B areas.” |

| Red | D “Hazardous” | HOLC described D areas as “characterized by detrimental influences in a pronounced degree, undesirable population or an infiltration of it.” It recommended that lenders “refuse to make loans in these areas [or do so] only on a conservative basis.” |

How Maps Became a Tool for Discrimination

The HOLC maps became a tool for widespread discrimination. Would-be homeowners in certain areas found it difficult or impossible to get a mortgage because capital was directed to White families living in green and blue neighborhoods—away from Black and other minority families in yellow and red communities. The rare loans that were available in redlined areas were very expensive, which made it even harder to buy a home and build wealth.

Unable to get regular mortgages, people of color who wanted to own a house were forced to resort to exploitatively priced housing contracts that massively increased the cost of housing and gave them no equity until their last payment was delivered. Chicago’s Contract Buyers League was formed in the 1960s by a group of inner-city residents to fight these practices.

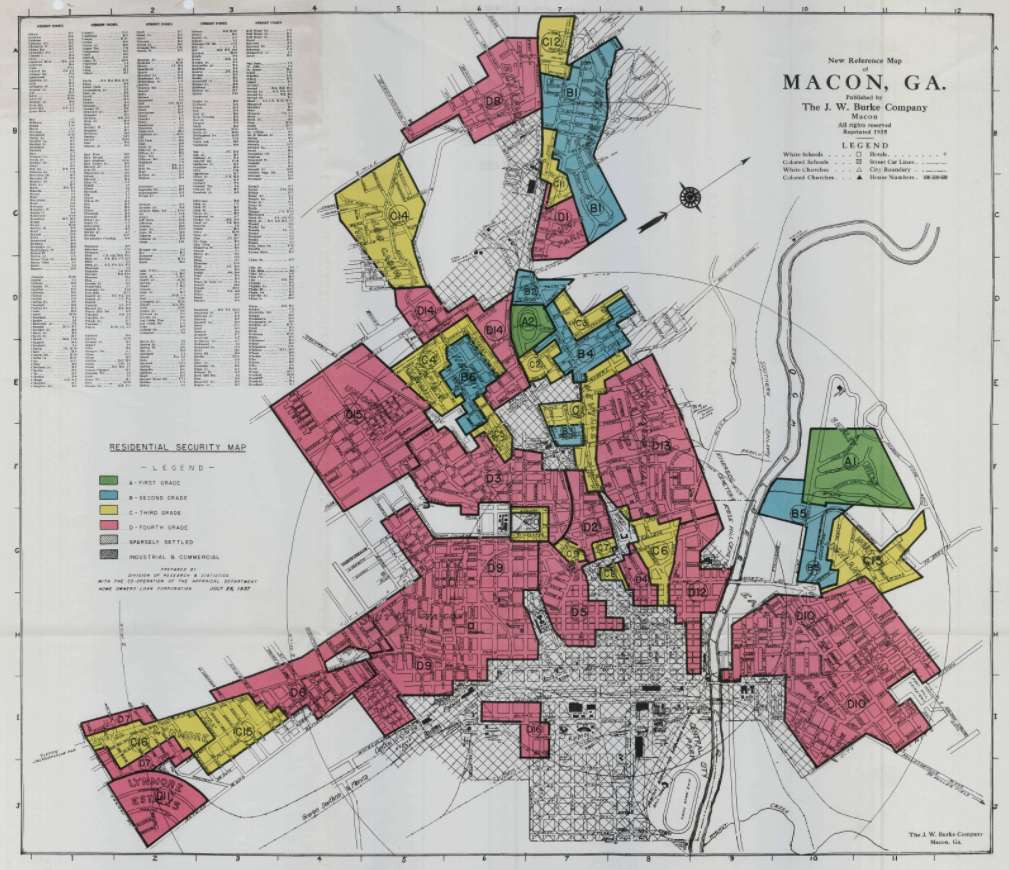

With nearly 65% of its neighborhoods marked in red, Macon, Ga., was the most redlined city in the U.S.

Image source: Mapping Inequality.

Here’s a list of the 10 cities with the highest percentage of neighborhoods marked “hazardous” in the 1930s, per a National Community Reinvestment Coalition (NCRC) study as reported by the nonprofit news website NextCity.com.

- Macon, Ga., 64.99%

- Birmingham, Ala., 63.91%

- Wichita, Kan., 63.87%

- Springfield, Mo., 60.19%

- Augusta, Ga., 58.70%

- Columbus, Ga., 57.98%

- Newport News, Va., 57.51%

- Muskegon, Mich., 57.24

- Flint, Mich., 54.19%

- Montgomery, Ala., 53.11%

Economic and Racial Segregation from Redlining Persists Today

The immediate effect of redlining was that residents in racial and ethnic minority neighborhoods couldn’t access capital to improve their housing (to buy or renovate) or for other economic opportunities. Of course, the impacts of redlining didn’t magically end when the FHA was passed in 1968. Instead, as a 2018 study by the NCRC showed, the economic and racial segregation created by redlining persisted in many cities. For example:

- 74% of neighborhoods that the HOLC graded as “hazardous” more than 80 years earlier remained LMI.

- 64% of HOLC’s hazardous-graded areas were still racial and ethnic minority neighborhoods.

Image source: Mapping Inequality (https://dsl.richmond.edu/panorama/redlining/#loc=5/39.1/-94.58).

By comparison, 91% of areas deemed “best” in the 1930s remained middle- to upper-income (MUI), and more than 85% were still predominantly White.

The median net worth of Black families is about 16% that of White families; Hispanic families’ median net worth is about 22% that of White families.

According to the Mapping Inequality project of the University of Richmond, “As homeownership was arguably the most significant means of intergenerational wealth building in the United States in the twentieth century, these redlining practices from eight decades ago had long-term effects in creating wealth inequalities that we still see today.”

The Lingering Legacy of Discriminatory Lending

Past redlining is one factor behind the persistent racial wealth gap in the U.S. And even though discriminatory lending practices are prohibited under the FHA, ECOA, and CRA, Black borrowers and those from other racial and ethnic minority groups remain at a disadvantage. These are a few of the lingering effects of redlining:

Higher Interest Rates

An analysis of nearly 7 million 30-year mortgages by the University of California at Berkeley found that Black and Latinx/Hispanic applicants were charged 0.08% higher interest rates compared with White borrowers, costing them $765 million in extra interest per year.

Lower Loan Approval Rates

In a 2020 mortgage study conducted by the Consumer Financial Protection Bureau, Black and Hispanic White borrowers had higher denial rates than non-Hispanic White and Asian borrowers. For Black loan seekers, the denial rate was 18.1%, and for Hispanic White loan seekers, it was 12.5%. By contrast, the denial rate for Asian applicants was 9.7%, and for non-Hispanic White applicants, it was 6.9%.

Lower Homeownership Rates

Discrimination has led to a significant homeownership gap between Blacks and Whites in the U.S. The national homeownership rate for Black families in late 2023 was 45.5%, compared to 74.5% for White families, according to the U.S. Census Bureau.

Lower Personal Wealth

According to a 2020 report from real estate firm Redfin, over the past 40 years, the typical homeowner in previously redlined neighborhoods has gained 52% less—or $212,023 less—in personal wealth from property value increases than homeowners in greenlined areas.

“Corporate Redlining” Hampers Black-Owned Businesses

Discrimination goes beyond mortgage lending. A 2020 analysis by The Business Journals found that White neighborhoods received roughly twice as much per person in small-business loans compared with Black neighborhoods. Similarly, predominantly White neighborhoods received, on average, about twice as many small-business loans per capita.

The report also noted that, since peaking before the 2008 financial crisis, the number of loans made to Black-owned businesses through the Small Business Administration’s 7(a) program decreased by 84%, compared to a 53% drop in 7(a) loans awarded overall.

The decline came despite other positive trends, including a 48% growth in the economy, an 82% rise in commercial loans, and a 101% increase in bank deposits. Orv Kimbrough, chair and chief executive officer at Midwest BankCentre, called this disparity “corporate redlining.”

Discrimination, whether seen in mortgage or small-business lending, has lasting effects. “When you don’t invest, you get social problems, you get crime, less education, all of which reduces the chances of people climbing the social and economic ladder,” noted Andre Perry, a fellow at the Brookings Institution who studies wealth creation and race.

If You Experience Lending Discrimination

Mortgage applicants and homebuyers who believe they have been discriminated against should contact the Office of Fair Housing and Equal Opportunity (FHEO) at the U.S. Department of Housing and Urban Development (HUD) or the Consumer Financial Protection Bureau (CFPB).

Small business owners who believe they have been discriminated against based on race, sex, or another protected category can submit a lending discrimination complaint online with the CFPB.

What is Redlining?

Redlining is the now-illegal discriminatory practice of denying credit to residents of certain areas based on their race or ethnicity. The term was coined by sociologist John McKnight in the 1960s, based on Home Owners’ Loan Corp. (HOLC) maps that marked racial and ethnic minority neighborhoods in red, labeling them “hazardous” to lenders.

Does Redlining Happen Today?

Redlining is illegal now. But the redlining that occurred in the past still contributes significantly to the racial wealth gap that persists today.

What Are the U.S. Fair Lending Laws?

Fair lending laws in the United States prohibit lenders from discriminating based on certain factors (such as an applicant’s race, color, national origin, or religion) during any aspect of a credit transaction.

What Are the Three Types of Lending Discrimination?

Federal law recognizes three types of lending discrimination. According to the Federal Deposit Insurance Corp. (FDIC), they are:

- Overt discrimination—when a lender blatantly discriminates based on a prohibited factor

- Disparate treatment—when a lender treats applicants differently based on one of the prohibited factors

- Disparate impact—when a lender applies a practice uniformly to all applicants, but the practice has a discriminatory effect on a prohibited basis and is not justified by business necessity

What Is the Racial Wealth Gap?

The racial wealth gap describes the difference in accumulated wealth held by different racial or ethnic groups. It reflects the generations-long inequality in access to financial and educational opportunities, income, and resources.

The Bottom Line

Lending practices have gradually become more equitable in the U.S. But more equitable is not equal. The residual effects of redlining—and the ongoing discrimination against people of color today—continue to perpetuate the country’s racial wealth divide. Three-quarters of neighborhoods redlined in the 1930s continue to struggle economically today and are much more likely than other communities to be home to lower-income, racial and ethnic minority residents. They are also more likely to be the target of subprime and predatory lenders.

There are other enduring negative outcomes, too. A 2020 study by researchers at the National Community Reinvestment Coalition, the University of Wisconsin-Milwaukee, and the University of Richmond reported that, “the history of redlining, segregation and disinvestment not only reduced minority wealth, it impacted health and longevity, resulting in a legacy of chronic disease and premature death in many high minority neighborhoods.” In fact, the study found, life expectancy is 3.6 years lower in formerly redlined communities than in communities that had received high grades from the HOLC.